One in five family loans sparks a feud that lasts years, according to a fresh LendingTree survey. Lending family money sounds noble, but it often backfires. Experts warn it strains bonds built over decades. With inflation squeezing wallets, more relatives are asking for cash—leading to record tensions. This guide lays out ironclad rules to protect your finances and holidays. Follow them, or risk turning Thanksgiving into a battlefield.

Assess Your Own Finances First

Before handing over a dime, check if you can afford the loss. Financial advisors stress treating it like a gift, not a loan. A 2023 LendingTree report found 36% of borrowers never repaid, leaving lenders high and dry. Crunch the numbers: Would losing this money derail your emergency fund or retirement? If yes, walk away. Dave Ramsey, debt guru, hammers this point: Only lend what you are willing to flush down the toilet.

Set Crystal-Clear Expectations

Verbally promising “pay me back whenever” invites disaster. Spell out terms from day one: amount, repayment schedule, interest rate if any. Use simple language. One borrower told NerdWallet, “We agreed on $500 monthly, but vague start dates led to endless fights.” Document everything. This prevents “I forgot” excuses and keeps emotions in check.

Put It in Writing—Every Time

A handshake deal crumbles under pressure. Draft a promissory note. Include principal, interest, due dates, and default consequences. Free templates abound online, but tweak for your state laws. Investopedia outlines a solid one here. Courts uphold these docs, shielding you if push comes to shove. Skip this, and you’re betting on goodwill alone.

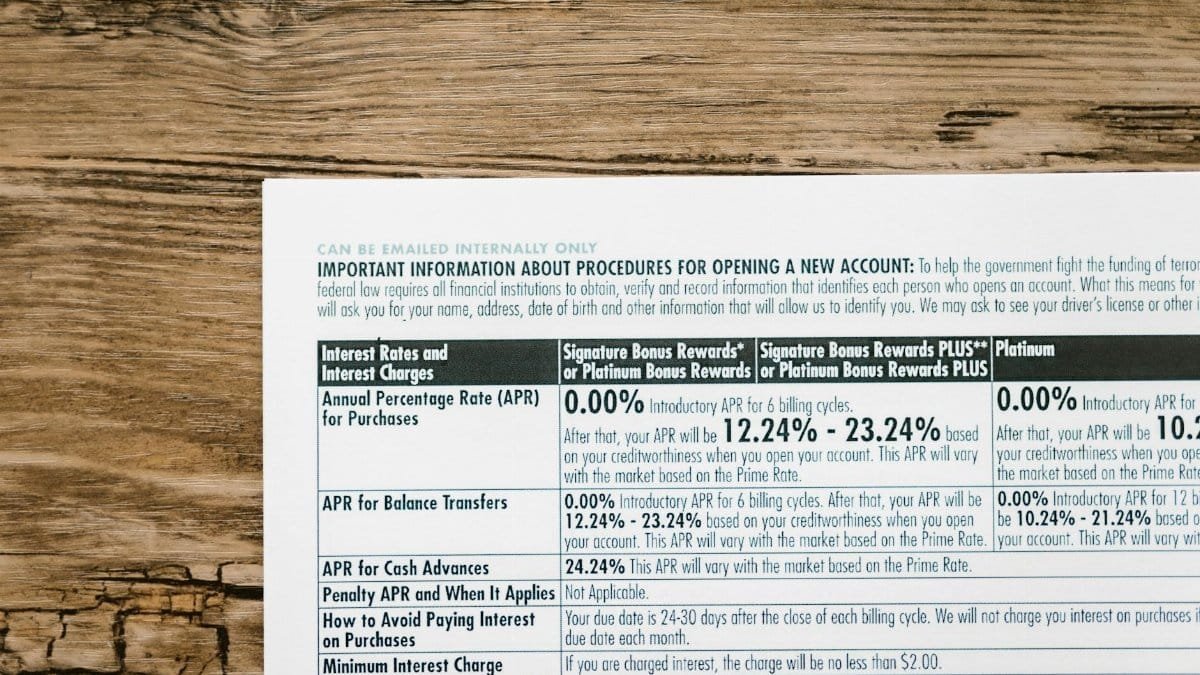

Charge Interest to Keep It Businesslike

Zero-interest loans blur lines between family and bank. The IRS minimum rate—called AFR—avoids tax headaches. For July 2024, short-term AFR sits at 4.74%. Charging it signals seriousness and compensates for inflation. Family member balks? That’s your cue it’s not a loan. NerdWallet details the pitfalls here. Zero percent often means zero repayment.

Know When to Just Say No

Not every sob story deserves your savings. Red flags: chronic poor money habits, no repayment plan, or history of flakes. Politely decline: “I love you, but I can’t risk my stability.” Therapists note “no” preserves relationships better than resentment. A CFP Board survey pegged 28% of lenders regretting yeses due to repeated asks.

Enforce Repayment Without Drama

Missed payment? Send a calm reminder email, referencing your note. No groveling or threats. Automate if possible via apps like Splitwise. If they ghost, pause further help. One lender shared: “I stopped chasing after month three—got partial back eventually.” Consistency builds respect, not grudges.

Handle Taxes Like a Pro

Forgive debt over $18,000 in 2024? Uncle Sam calls it income for the borrower. Lenders report interest earned on Schedule B. Track meticulously with apps like Mint. Consult a tax pro for forgiven amounts—they’re taxable gifts. Mess this up, and audits loom.

Legal Safeguards You Can’t Ignore

Loans over $600? File Form 1099-INT if interest flows. Big sums might need notarization. In disputes, small claims court favors written agreements. State usury laws cap rates—California limits at 10% for non-banks. Research yours via Nolo.com guides. Protection beats regret.

Alternatives That Save Face

Can’t lend? Suggest cosigning a bank loan (rarely wise) or apps like Prosper for peer funding. Nonprofits offer aid: Modest Needs grants emergency cash. Help job hunt or budget instead. This shifts focus from your wallet to solutions, dodging entitlement traps.

Lessons from Those Who Nailed It

Success stories prove rules work. A Texas dad lent his son $20K for a truck, with 5% interest and biweekly pulls from paychecks. Fully repaid in 18 months—no rift. Another capped at $1K gifts yearly, scripting IOUs for larger asks. Patterns? Boundaries and paperwork win. Experts say these outliers thrive by treating kin like clients.

Lending family money tests loyalty like nothing else. Stick to these rules: vet finances, document deals, enforce terms. Holidays stay merry, relationships intact. Ignore them, and you’re funding feuds. Smart money stays in the family—without the fallout.

Natasha is the heart of our exploration into conscious connection. Applying principles from multiple counseling courses in her own life, she guides you to cultivate stronger, more joyful bonds.

Disclaimer

The content on this post is for informational purposes only. It is not intended as a substitute for professional health or financial advice. Always seek the guidance of a qualified professional with any questions you may have regarding your health or finances. All information is provided by FulfilledHumans.com (a brand of EgoEase LLC) and is not guaranteed to be complete, accurate, or reliable.